US-Japan Tax Treaty: What American Expats and Businesses Need to Know in 2026

The US Japan tax treaty is a bilateral agreement that prevents you from paying tax twice on the same income.

If you are a US citizen living in Japan, a Japanese national earning income in the United States, or a business operating across both countries, this treaty determines which country gets to tax each type of income you earn.

This guide breaks down the treaty's key provisions, explains how double taxation is eliminated, and shows you how to claim the benefits you are entitled to.

What is the US-Japan tax treaty?

The US-Japan tax treaty is a bilateral agreement between the two countries that allocates taxing rights on income earned by residents and citizens of either nation.

The two primary goals of the treaty are to:

Eliminate double taxation on income earned by individuals and businesses in both countries

Prevent tax evasion and fiscal evasion through information exchange between the competent authorities of each country

The treaty follows the OECD Model Tax Convention framework and covers income tax, capital gains, dividends, interest, royalties, pensions, social security benefits, director's fees, and other categories of income.

👉 The full US-Japan tax treaty summary from the Ministry of Finance, Japan.

Who does the treaty apply to?

The US Japan tax treaty applies to individuals and entities that are tax residents of one or both countries.

US residents and US citizens (including US expats living abroad) are covered, as are Japanese nationals and foreign residents of Japan.

Japan classifies residents into three tiers:

Permanent residents (5+ years in Japan out of the past 10, taxed on worldwide income)

Non-permanent residents (1 to 5 years, subject to remittance based taxation on foreign source income)

Non-residents (less than one year, taxed only on Japan source income).

If both countries consider you a tax resident, the treaty provides tie-breaker rules based on permanent home, center of vital interests, habitual abode, and nationality, in that order.

How the treaty eliminates double taxation

Without the treaty, the same income could be taxed in full by both Japan and the United States. The treaty addresses this by allocating taxing rights for each type of income to one country or the other, or by capping the tax rate one country can charge.

The primary mechanisms for avoiding double taxation are:

Foreign tax credits

If you pay Japanese taxes on income that is also taxable in the US, you can claim a foreign tax credit on your US tax return (Form 1116) to offset your US tax liability.

This is the most common tool US expats use to eliminate double taxation.

For most Americans in Japan, the foreign tax credit works better than the Foreign Earned Income Exclusion (FEIE) because Japan's tax rates are generally higher than US rates.

Reduced withholding rates

The treaty caps or eliminates withholding tax on cross-border payments of dividends, interest, and royalties. This means the country where the payer resides cannot tax the full amount at its domestic rate.

Exemptions for specific income types

Certain categories of income are taxable only in one country. For example, income from government service is generally taxable only by the government that employs you.

The saving clause: A critical exception

The saving clause is one of the most important and misunderstood parts of the US-Japan tax treaty.

Under Article 1(4), the saving clause allows each country to tax its own citizens and residents as if the treaty did not exist.

This means the US preserves the right to tax US citizens on their worldwide income regardless of what the treaty says.

Even if a treaty article states that a certain type of income is taxable only in Japan, the saving clause lets the US tax it anyway for US citizens.

There are exceptions to the saving clause. The following treaty articles are not subject to it:

Social security benefits (Article 17)

Government service income for non-citizens (Article 18)

Certain student and trainee provisions (Article 19)

The mutual agreement procedure

Understanding the saving clause is essential for US expats. It is the reason that the foreign tax credit, rather than a treaty exemption, is the primary tool for reducing US tax liability on income earned in Japan.

Income tax provisions: What gets taxed where

The treaty establishes specific rules for different categories of income. Here is how the major types of income are treated.

Employment income (wages and salaries)

Under Article 14, wages and salaries earned by a US resident working in Japan are generally taxable only in the US unless:

The employee is present in Japan for 183 days or more in any 12-month period

The employer is a Japanese company (or has a permanent establishment in Japan)

The remuneration is paid by or on behalf of an employer in Japan

If any of these conditions apply, Japan can also tax the employment income.

Self-employed individuals follow similar rules under the business profits article.

Business profits and permanent establishment

Under Article 7, a US company is only taxable in Japan on business profits if it carries on business through a permanent establishment in Japan.

A permanent establishment includes a fixed place of business such as an office, branch, factory, or construction site that lasts more than 12 months.

If a US company does have a permanent establishment in Japan, only the profits attributable to that establishment are subject to Japanese taxation. The same rule applies in reverse for a Japanese company operating in the US.

Dividends (article 10)

Dividends paid by a Japanese company to a US resident are subject to withholding tax, but the treaty caps the rate:

0% if the beneficial owner is a company that has held at least 50% of the voting stock for 6 months or more (the ownership threshold was met for 12 months before the 2013 Protocol reduced it to 6)

5% if the beneficial owner is a company that owns at least 10% of the voting stock

10% for all other dividends paid to US residents

Without the treaty, Japan's domestic withholding rate on dividends would be approximately 20.42%.

Interest (article 11)

Under the amended treaty, interest paid on most cross-border loans and bank deposits is subject to 0% withholding tax. This is a significant benefit introduced by the 2003 treaty and expanded by the 2013 Protocol.

The exception is contingent interest, which is interest whose amount depends on the receipts, sales, income, or profits of the debtor. Contingent interest is taxed at 10%.

Royalties (article 12)

Royalties paid for the use of intellectual property between the two countries are exempt from withholding tax at the source. The 0% rate applies whether the payer is a US company paying a Japanese resident or a Japanese company paying a US resident.

Capital Gains (article 13)

Capital gains from the sale of real property are taxable in the country where the property is located. If you sell an apartment in Tokyo, Japan gets to tax the gain.

Capital gains from the sale of stocks and other financial assets are generally taxable only in the country of residence.

A US resident who sells shares in a Japanese company will typically pay capital gains tax only in the US. However, if the shares derive more than 50% of their value from real property in the other country, that country may also tax the gain.

Pensions and retirement income

Private pensions and annuities are generally taxable only in the country of residence.

However, because the saving clause applies to private pensions, the US can still tax pension income received by US citizens regardless of where they live.

Social security benefits

Social security benefits are taxable only in the country that pays them. US Social Security payments to a US citizen in Japan are taxable only in the US. Japanese social security payments to a Japanese national are taxable only in Japan. This provision is one of the exceptions to the saving clause.

US-Japan totalization agreement

Avoiding dual social security taxes

Separate from the income tax treaty, the US-Japan totalization agreement addresses social security taxes. Without this agreement, Americans working in Japan would pay social security taxes to both countries at the same time.

The totalization agreement, which became effective on October 1, 2005, works as follows:

Temporary assignments (5 years or less): If a US employer sends you to Japan for up to 5 years, you continue paying only US Social Security. You need a Certificate of Coverage from the US Social Security Administration to prove your exemption from Japanese social security taxes.

Long-term or local hires: If you are hired locally in Japan or your assignment exceeds 5 years, you pay into Japan's pension system instead.

Self employed workers: Self employed individuals pay social security taxes only in their country of residence.

The agreement also lets you combine work credits from both countries to qualify for benefits. If you have social security credits in both the US and Japan but not enough in either country alone, the totalization agreement can help you meet the minimum requirements for social security benefits in one or both countries.

How to claim treaty benefits

To take advantage of the US-Japan tax treaty, you need to file the right forms in both countries.

In the United States

Form 1116: Claim foreign tax credits for Japanese taxes paid on income also taxed by the US

Form 8833: Disclose your treaty-based position if you are claiming a specific treaty benefit on your US tax return

Form 1040: Report worldwide income on your standard US income tax return

FBAR (FinCEN Form 114): Report foreign bank accounts if your combined balances exceed $10,000 at any point during the tax year

Form 8938: Report specified foreign financial assets above the reporting threshold under FATCA

In Japan

To claim reduced withholding rates under the treaty, file the relevant application with Japan's National Tax Agency (NTA) through the withholding agent (the payer) before the payment date. Without filing the NTA treaty application before the day of payment, Japan will withhold at its full domestic rate.

For Japanese income tax filing, residents of Japan file form the annual tax return (kakutei shinkoku) by March 15 of each tax year.

Key treaty benefits at a glance

Here is a summary of the withholding tax rates under the US Japan tax treaty compared to each country's domestic rates:

Income Type |

Treaty Rate |

Japan Domestic Rate (Without Treaty) |

|---|---|---|

Dividends (50%+ ownership, 6+ months) |

0% |

~20.42% |

Dividends (10%+ ownership) |

5% |

~20.42% |

Dividends (all other cases) |

10% |

~20.42% |

Interest (general) |

0% |

~20.42% |

Contingent interest |

10% |

~20.42% |

Royalties |

0% |

~20.42% |

Common mistakes US expats make

Filing taxes across two countries is complex. Here are the errors that cost US expats the most money:

Choosing FEIE when the Foreign Tax Credit is better. Japan's income tax rates are higher than US rates for most brackets. The Foreign Tax Credit (Form 1116) usually eliminates your entire US tax liability and can create a carryforward. The FEIE wastes those excess Japanese taxes.

Not filing the NTA treaty form before payment. If you do not file the Japan National Tax Agency treaty application through the withholding agent by the day before payment, Japan withholds at its full statutory rate. You can file for a refund later, but the process takes months.

Missing FBAR and FATCA deadlines. Penalties for not reporting foreign financial accounts start at $10,000 per violation. If you have bank deposits in Japan, you likely need to file FinCEN Form 114.

Ignoring pension treaty provisions. US citizens in Japan sometimes pay tax on pension income in both countries when the treaty could reduce the burden. Understanding whether the saving clause applies to your specific pension type matters.

Not filing a US tax return at all. The US taxes its citizens on worldwide income regardless of where they live. Even if you owe nothing after credits, you are required to file form 1040.

How remittance-based taxation affects the treaty

If you are a non-permanent resident of Japan (a foreigner who has lived in Japan for less than 5 of the past 10 years), you benefit from remittance-based taxation. Under this system, Japan only taxes your foreign-source income to the extent you remit funds to Japan during the same tax year.

This creates a planning window for US expats.

Foreign source income that stays outside Japan is not subject to Japanese taxes during your non-permanent resident years.

The treaty interacts with this by allowing certain foreign source income, like capital gains from overseas brokerage accounts, to remain outside Japan's taxing reach if you do not remit the proceeds.

Once you become a permanent resident (after 5 years), Japan taxes your worldwide income, and the foreign tax credit becomes your primary tool for preventing double taxation on the same income.

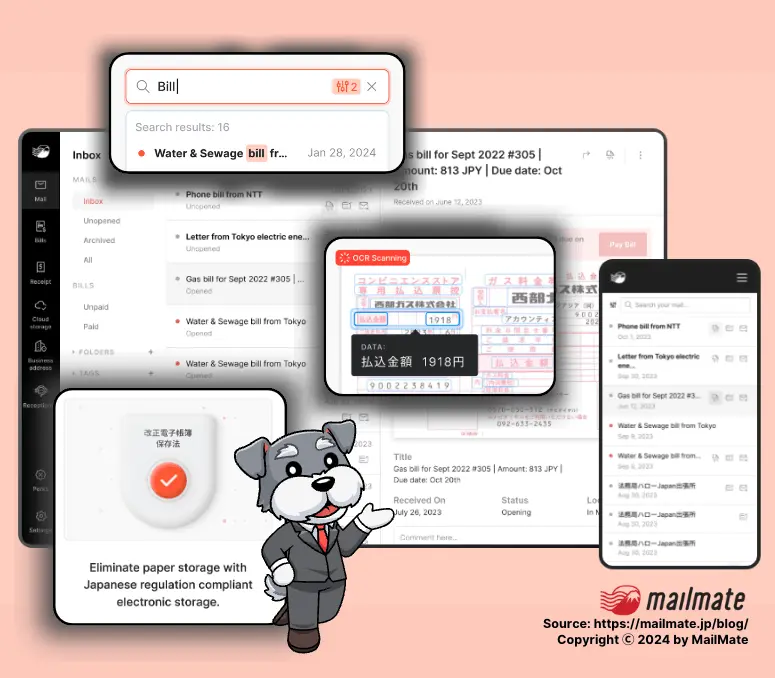

How MailMate helps you stay on top of Japanese tax obligations

If you are a US citizen or business owner managing affairs in Japan from overseas, staying compliant with Japanese taxation requirements often means dealing with official mail from Japan's National Tax Agency, municipal tax offices, and pension authorities.

That mail arrives in Japanese, on Japanese timelines, and missing a deadline can mean penalties.

MailMate is a virtual mailbox service that scans, translates, and digitizes your Japanese mail so you can access it from anywhere in the world.

When a tax notice from the NTA or a payment slip from your local ward office lands in your Japanese mailbox, MailMate scans it and provides an English translation. You see the document the same day, not weeks later.

For property owners, MailMate also handles bill payments for things like fixed property tax, utilities, and real estate acquisition tax.

If you own real property in Japan but live in the US, MailMate can pay your bills and file the necessary paperwork with your local tax office on your behalf.

MailMate's tax agent service covers fixed property tax and real estate acquisition tax filings, and its ERRL-compliant document storage means your Japanese tax records are organized and accessible at tax return time.

Whether you need to reference a withholding statement for your US tax return or provide documentation to your CPA, everything is stored digitally in one place.

Frequently Asked Questions

Does the US have a tax treaty with Japan?

Yes. The US and Japan have a comprehensive income tax treaty that has been in force since 1972, with major updates in 2003 and 2013. The treaty allocates taxing rights between the two countries and reduces or eliminates withholding tax on dividends, interest, and royalties to prevent double taxation.

How does the saving clause affect US citizens in Japan?

The saving clause in Article 1(4) allows the US to tax its own citizens as if the treaty does not exist, with limited exceptions. This means US citizens cannot use most treaty provisions to avoid US tax. The primary exceptions include social security benefits and certain government service income. US citizens rely on the foreign tax credit rather than treaty exemptions to reduce their US tax liability.

What is the withholding tax rate on dividends under the treaty?

The rate depends on the ownership threshold. If a company owns 50% or more of the voting stock for at least 6 months, dividends paid are subject to 0% withholding. If a company owns at least 10%, the rate is 5%. For all other dividends paid to residents of the other country, the rate is 10%.

Do I need to file a US tax return if I live in Japan?

Yes. The US requires all citizens and green card holders to file a federal income tax return regardless of where they live, as long as their income exceeds the filing threshold for their status. You must report your worldwide income earned in Japan and elsewhere on Form 1040. You can use the foreign tax credit or the FEIE to reduce or eliminate your US tax liability.

What is the US-Japan totalization agreement?

The US Japan totalization agreement is a separate bilateral agreement from the income tax treaty. It prevents you from paying social security taxes to both countries at the same time. If you are temporarily assigned to Japan by a US employer for up to 5 years, you continue paying only US social security. Local hires and long-term residents pay into Japan's system. The agreement also lets you combine work credits from both countries to qualify for social security benefits.

Can I use the treaty to avoid capital gains tax on Japanese real property?

No. Capital gains from the sale of real property in Japan are taxable in Japan regardless of your country of residence. The treaty confirms that the country where real property is located has the right to tax gains from its sale. However, you can claim a foreign tax credit on your US tax return for the Japanese capital gains tax you pay.

This article is for informational purposes only and does not constitute tax, legal, or financial advice. Tax laws and treaty provisions can change. Consult a qualified tax professional for advice specific to your situation.

Read also:

👉 Japan Tax Representative Form + How to Appoint a Tax Agent

👉Japan Inheritance Tax: The Complete Guide

花太多時間處理日本郵件?

虛擬郵箱 + 翻譯服務每月僅需 3800 元起。30 天退款保證。